3 Steps to Success for Spouses When There is a Divorce with a Business Involved

When a divorce involves a business, husbands and wives must carefully navigate the process

{kind=link}

You have a divorce with a business involved and you have many questions

That is normal. Did you ask yourself one or more of these questions?

- "Will my spouse really get half of my business?"

- "How will a court decide what my business is worth?"

- "How am I supposed to pay spousal support and buy out my spouse from the business?"

- "Am I really going to spend a fortune on lawyers and forensic accountants just to figure out what this business is worth?"

When you have a divorce that involves a business, knowledge is your greatest ally

We wrote this article for those husbands and wives who operate the business although it will benefit the non-operator spouse just as much. What we provide here is not legal advice and not intended to apply to your specific situation.

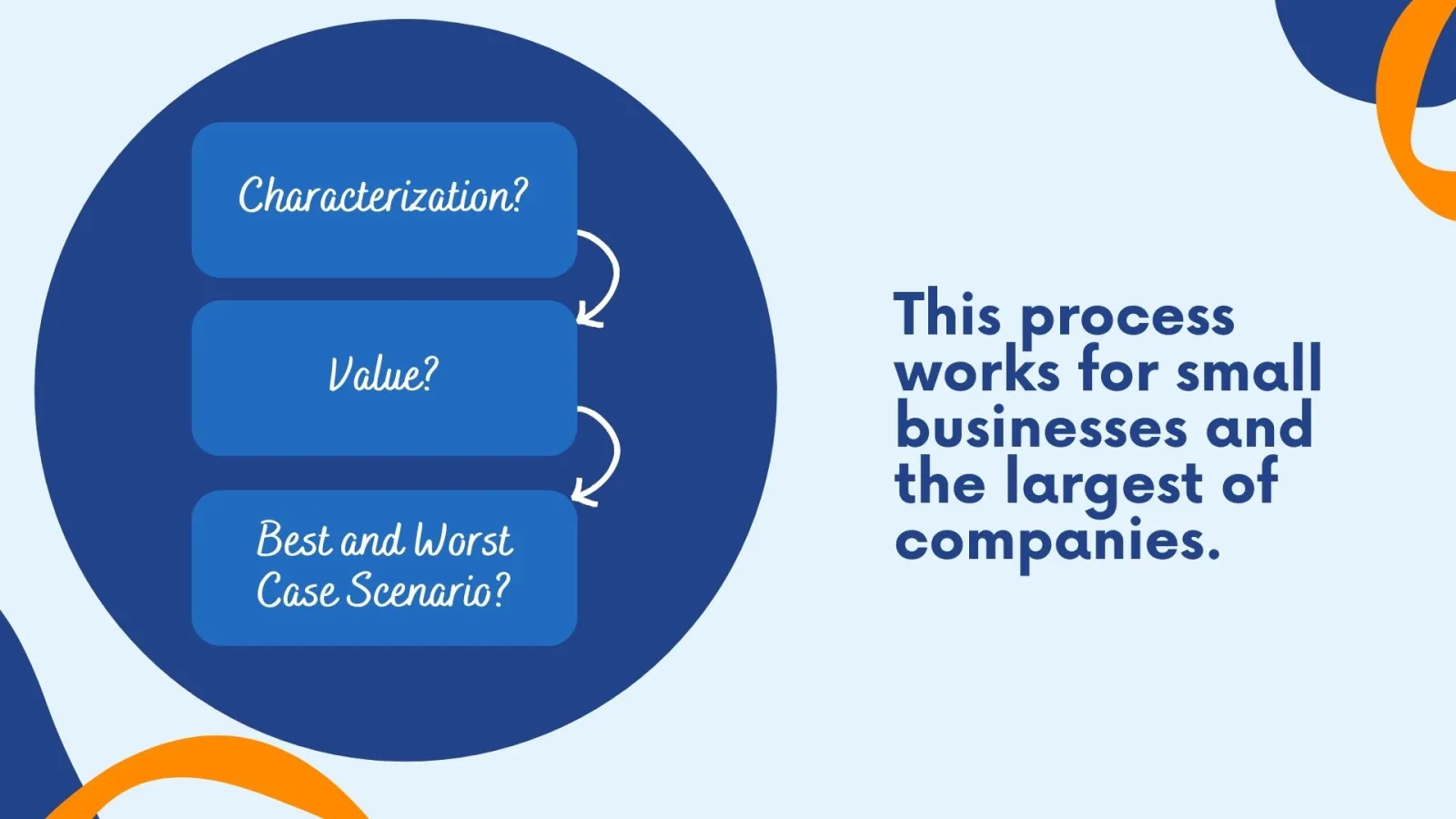

Three-step process to a successful conclusion of a divorce with a business

We have a three-step process as to every divorce case that involves a business. This process is effective no matter the size of the business or the type of entity involved.

Here is a chart that explains the process. We will explain this chart in more detail below.

Is the business community property, separate property or a combination?

There are several factors spouses must look at to determine a business' characterization.

If the spouses started the business during the marriage, regardless of who operated the business, and the business acquisition did not result from a gift, inheritance or other separate sources, there may be less analysis.

Like any other property, a divorce that involves a business starts with a look at the date of acquisition and source of acquisition.

What about a business started prior to the marriage?

If the divorce involves a business started before marriage, one spouse may have separate property arguments.

Contrary to urban legend that we sometimes hear from spouses, the fact a spouse started the business prior to the marriage does not automatically mean the business is 100% that spouse's separate property.

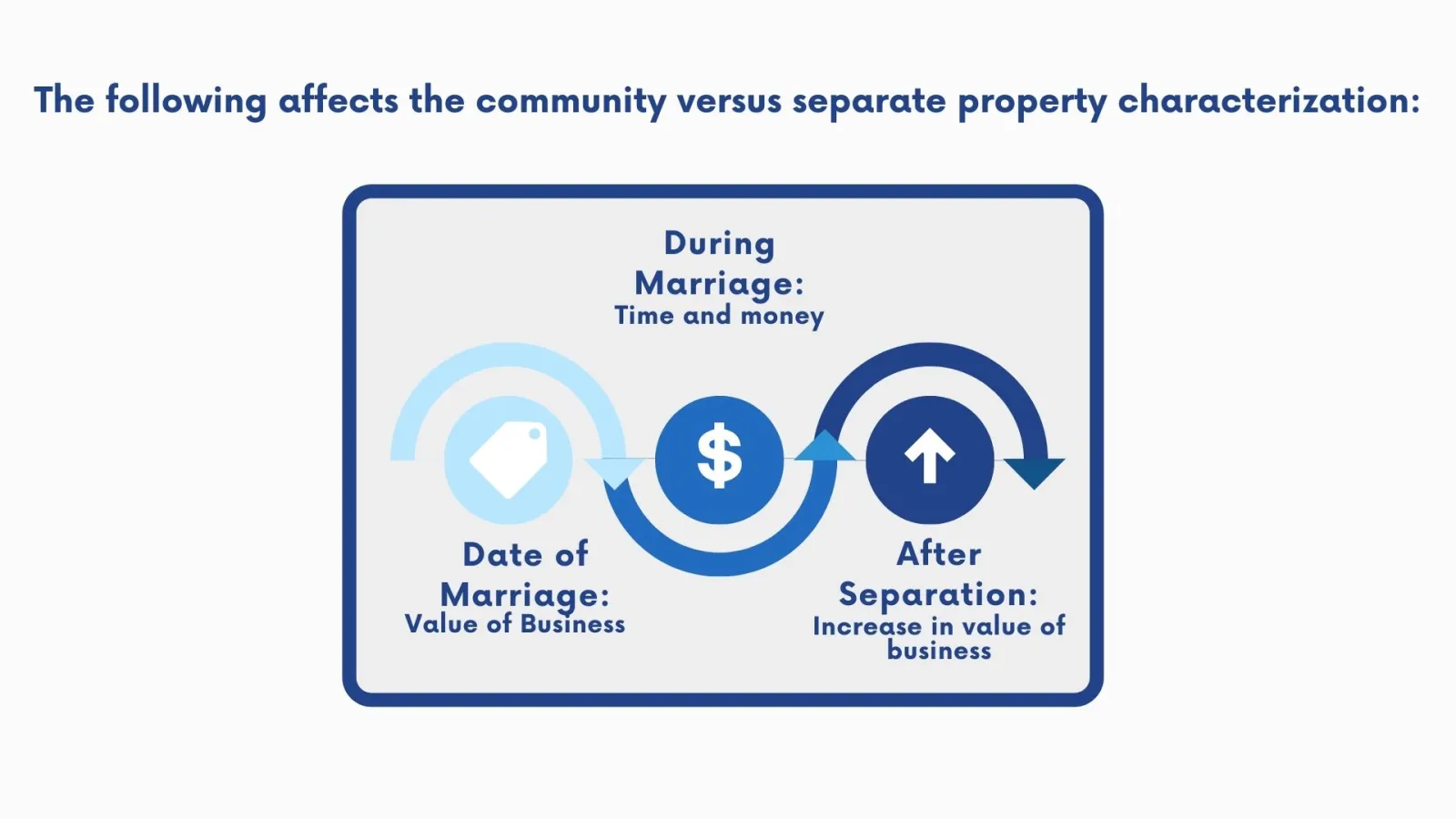

The following affects the community versus separate property characterization.

To summarize, you have:

- The business' value at the time of the marriage,

- The nature and extent of the operating spouse's contribution of time and money to the business during the marriage,

- The business' value on the date of separation and/or later at the time of the trial or final resolution, and

- Other factors.

A divorce that involves a business becomes more complicated as the facts regarding acquisition and contribution toward the business prior to the marriage and after the marriage become more complex.

The business' size is less a characterization issue and more a valuation issue, which we will discuss next.

Related Helpful Articles on California Divorces

What is the value of the business?

If there is an accurate way to value a business without an expert's help, I am not aware of it. A business, unlike a car, does not have a guide where you can look at a few factors and see its value. There is no online progra for businesses.

For many businesses, the largest component of value may be the business' goodwill.

A business' goodwill means the expectation of continued public patronage

Forensic accountants and experts specific to a business' industry help determine a business' goodwill. The more established a business is and the more it relies on its brand or reputation, the greater the goodwill.

We look at the following when we determine goodwill. However, these are not the only factors.

Let's break down the "goodwill" factor into more detail.

Goodwill is not the only factor, but it is an important one when valuing the business during the divorce.

Other factors are the business' earnings, expenses, profit, assets, debts and liabilities and more factor into the valuation process.

But first, let's look at goodwill in more detail.

The location of the business.

A business' location in a busy metropolitan city may affect goodwill differently than one more remote.

A business that operates exclusively online may have a different goodwill than a business with a physical location.

The amount of patronage the business receives.

Volume of business is often directly related to its popularity and patronage.

The personality of the business owner or operator and especially in service-based businesses.

For some businesses, the business owner or operator is the "brand."

The business' past and ongoing earnings.

Typically, the greater the earnings, the greater the profit.

Some businesses have nice profit margins and keep more of the money they earn. Others have tighter margins.

The business' reputation, which is often part of its brand and recognition.

Is the business well known? Is it a household name? Is it a niche business within a niche industry or does it appeal to a greater number of consumers?

The business' longevity.

The longer the business has been around and has been successful, the more likely that success will continue.

The loyalty of the business' customers and especially if there is repeat business.

Is this a business to which customers return?

Some spouses foolishly procrastinate the business valuation process

While some spouses foolishly resist this process, it is in our opinion, without exception, best to start the business valuation process early in the divorce.

When you have a divorce with a business involved, procrastinating may be your enemy. It is the equivalent of, as kids, cleaning under the refrigerator when you have homework to get done.

The homework is not going away and no matter how much you try to avoid it, you have to do it unless you want to fail that class. If you want to potentially fail at a divorce with a business involved, procrastinate at the valuation process.

If you are the person who operates the business and you are procrastinating, you probably hold out some hope your spouse will not require the valuation process and you can somehow negotiate your way to reasonable deal.

If you are the spouse who is not operating the business, you probably hope for the same thing.

Although I am sure every experienced family law attorney has at some point run across a client who refuses to listen to advice (we are no exception), the only person you may be hurting is yourself both in the short and long run.

It is best to value the business so you are making more informed choices.

Are very short marriages the exception?

There are probably situations where spouses may reach a resolution without the need for a forensic accountant.

While the situations are rare, one that comes to mind is a very short marriage. One example may be a marriage under six months where it is clear:

- The business started well before the marriage, and

- Could not have had any increase in value during the marriage.

Even in such situations, it is best to at least consult with a forensic accountant but how much money spouses pour into that process may vary from one situation to another.

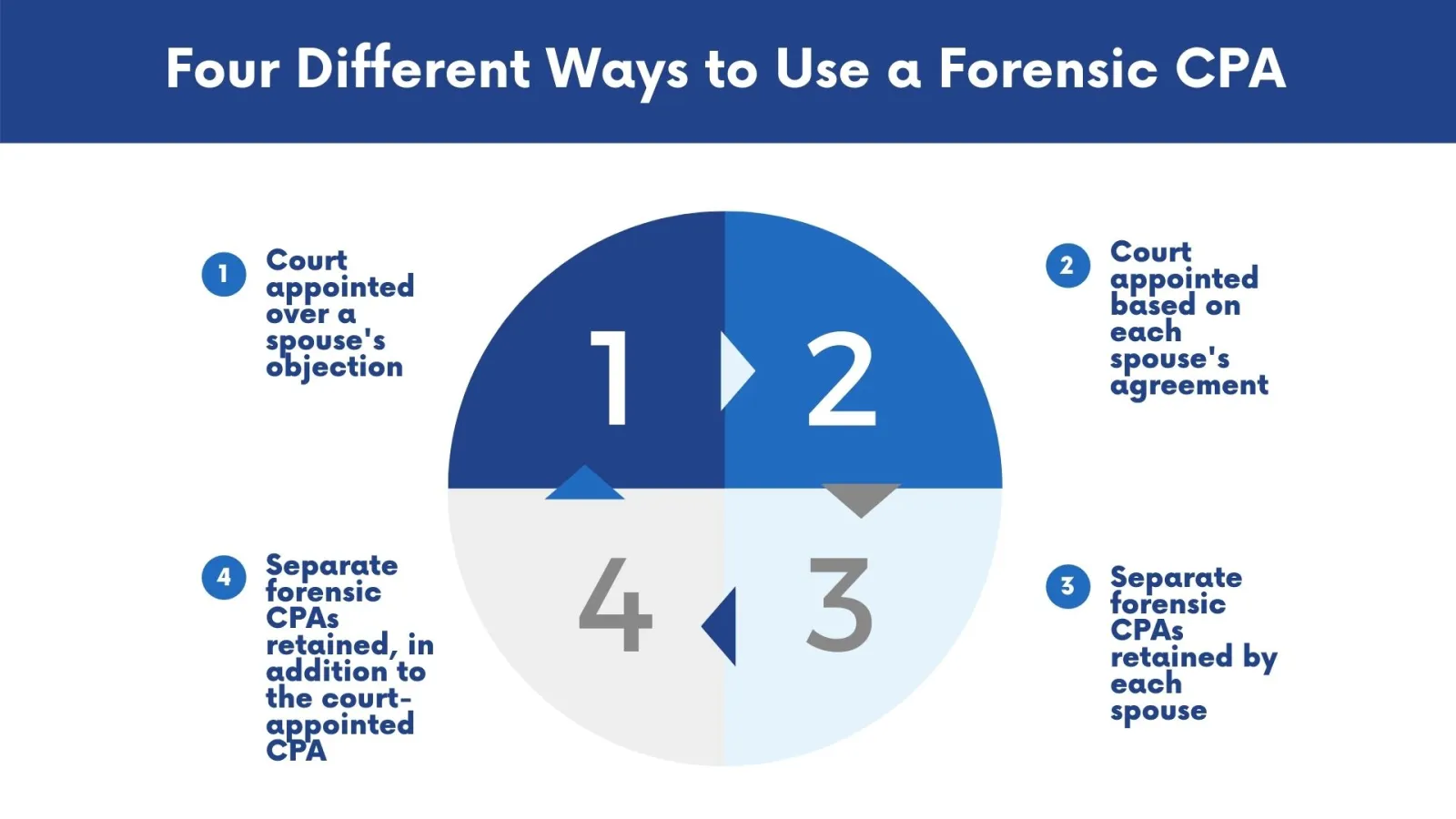

What are the best and worst-case scenarios regarding division of the business?

Some spouses hire their own forensic accountant to conduct the business valuation. This is usually the wiser choice.

Some spouses agree on a joint forensic accountant. This only makes sense in certain, limited cases. One example is a business that does not have significant value and it is unlikely there will be a strong difference of opinion on that business's value.

Here are the four scenarios we see.

The court has the power to order and appoint a forensic accountant

The court has the power to appoint a forensic accountant to prepare a report on issues such as income available for support (also called controllable cash flow) and business valuation. Such experts are often appointed pursuant to Evidence Code 730. They are sometimes called 730 Evaluators.

If the court makes such an order, it is usually the result of one spouse's request for such an order. The court does not have to make such an order and a spouse (especially the business operator) can and sometimes should resist the court appointing its own expert.

Forensic accountants and experts do not always agree on the value of the business

What does the above tell you? It tells you there can be a significant difference of opinion between experts such as forensic accountants regarding a business' value.

Our family law firm has seen situations where two separate forensic accountants came back with values hundreds of thousands of dollars apart for the same business.

It is conceivable two forensic accountants can even be millions of dollars apart in certain scenarios with very high valued businesses.

The spouses and attorneys must collaborate regarding options

For this reason and others, each spouse and his or her attorney should discuss options available to them.

This is true regardless of whether the divorce with a business involved settles or proceeds to trial.

Much of that discussion centers on this difference of opinion in value

Naturally, if the forensic accountants agree on the value of the business, the issue is not the value. The issue then becomes how the spouses will divide the community property portion through a buyout or "division in kind".

If a buyout, this can be through a cash payment, an installment plan or even an offset against other community property assets.

If there is a significant difference of opinion in the business' value, each spouse and his or her lawyer should analyze, (a) whether one or both forensic accountants overreached in their analysis, and (b) which report is more reliable.

The spouses should also consider whether a compromise makes sense if neither can withstand the potential for the court to order their worst-case scenario at trial. Remember trial is a risk. You take control out of your mutual hands and give it to a judge to make the decision.

Ready for a strategy session on the business in your divorce?

Our divorce and family law firm has offices in Orange County, Los Angeles and San Diego.

We provide representation to clients who have cases in each of the seven Southern California counties.

Contact us today for an affordable strategy session.

Your Strategy Session

About your strategy session

Southern California Offices

Locations

Our Services and Fees

Frequently asked questions

Strategy sessions are designed for the serious client. This is your money & your future financial security. That is why we are intense and result-focused, and why you should be too.