{kind=link}

Learn about the tax deductibility of legal fees in a divorce

This is a guest article from David Ellis, CPA. The opinions expressed in this article are that of Mr. Ellis and not our family law firm. Nothing contained in this article is intended to be tax advice or advice of any other kind.

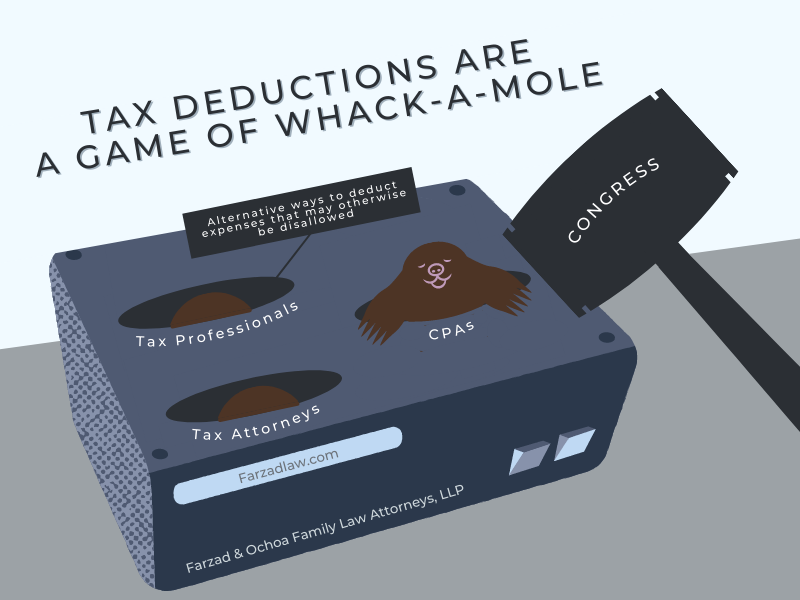

If you have had a mole in your yard, you have probably experienced the frustration of filling in one hole, only to discover fresh perforations the next day. Although it is not a flattering analogy, I often feel it is the same with tax deductions.

The CPAs, Tax Attorneys, and various other tax professionals stand in for the moles. The holes are alternative ways to deduct expenses that may otherwise be disallowed. The homeowner is Congress since it is the progenitor of the tax laws.

Take for example the matter of the deductibility of legal fees related to divorce

Taxpayers have generally been able to deduct certain legal fees associated with divorce as a miscellaneous itemized deduction practically since George Washington was in high school. The deduction did have some pesky limitations, but the general consensus was part of something is better than all of nothing.

Then along came the Tax Cuts and Jobs Act (TCJA) which eliminated most miscellaneous itemized deductions, including legal fees for tax years 2018 to 2025 (inclusive). However, for the tax mole who knows where to dig, there are loopholes to be found.

Some history on tax deductibility of legal fees

Prior to the TCJA a qualifying taxpayer could deduct divorce related legal fees, provided such fees were paid for the production or collection of income (for example—securing alimony) or obtaining tax advice.

Legal fees paid to resist alimony have never been deductible. Moreover, those legal fees that were deductible generally had to be deducted as miscellaneous itemized deductions subject to a 2% limitation of Adjusted Gross Income (AGI).

For example, if your adjusted gross income was $200,000, the first $4,000 ($200,000 x 2%) of the divorce related legal fees paid in any given year would be non-deductible. After getting past the 2% of AGI hurdle, your overall itemized deductions had to exceed the standard deduction.

This did not always happen, especially with low-income taxpayers. In such cases the tax deductibility of the legal fees was simply lost.

Even for high income taxpayers with abundant Itemized Deductions that exceeded the 2% of AGI hurdle there could still be problems.

Divorce related legal fees were considered Miscellaneous Itemized Deductions and were therefore classified as so called "Tax Preference Items". In the normal world you would think anything described using the term "preference" would be a good thing.

However, in the arcane upside-down world of taxes, a Tax Preference Item is not a good thing. In fact, it is a very bad thing—at least for the taxpayer. This is because Tax Preference Items when present above certain thresholds will trigger the Alternative Minimum Tax (AMT).

The AMT is basically a set of rules within the tax code to ensure that taxpayers with certain types of deductions (aka Tax Preference Items) will pay a minimum level of income tax. In other words, it is Congress' version of "heads I win—tails you lose".

Divorce-related legal fees to procure alimony and tax advice could thus trigger the AMT tax

Sadly, the AMT can be easy to overlook for professionals who do not inhabit the tax swamp on a daily basis, and sometimes even for those who do.

So, even prior to the TCJA deducting divorce related legal fees was no walk in the park. The TCJA put this deduction out of its misery on the federal level for tax years 2018 to 2025 (inclusive), with respect to deducting legal fees as miscellaneous itemized deductions.

For those years ALL miscellaneous itemized deductions subject to 2% of AGI have been declared non-deductible. Thus, for the time being this hole in the tax code has been filled in; but a crafty tax mole can usually find another yard in which to dig.

First, and most obvious, legal fees may still be deductible as miscellaneous itemized deductions on the state level in states that never conformed to the TCJA.

In California, which did not conform, the top tax rate is 13.3%, so the tax effect of this deduction may not be trivial. Likewise, sometimes one spouse will pay the other spouse's legal fees. It is possible that such payments may be classified as alimony for state purposes.

However, one must be certain that all of the requirements for alimony are met under the rules prior to the TCJA.

Deducting divorce related legal fees as alimony for purposes of obtaining a state tax deduction may be nice, but there are yet bigger tax saving holes to be dug by the tax mole finding himself in the right neighborhood.

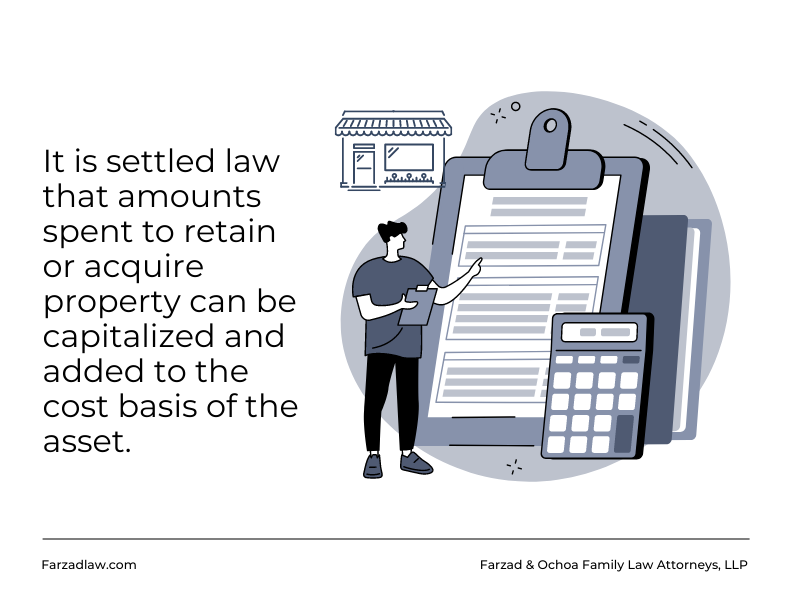

For example, it has been well established that amounts spent to retain or acquire property can be added to the cost basis of such property (capitalized). These amounts can include legal fees.

Costs that are capitalized onto property can result in depreciation deductions

For example, suppose you spend $100,000 in legal fees defending the title to an apartment building. Since the statutory depreciation period for residential rental property is 27.5 years, you will be able to deduct $3,656 per year of the fees, subject to whatever limitations apply to your particular situation.

As an added bonus any of the legal fees that are not depreciated will generally decrease the capital gains tax you pay if and when you sell it, since any increase in basis will reduce the gain of the sale.

These are nice tax deductions of course, but "nice" can be compared to when your grandma makes you cookies, its ok as far as it goes, but it's not in the same category as kissing the Prom Queen. However, being able to FULLY deduct your divorce related legal fees against your other ordinary income might even be better than kissing the Prom Queen - at least for a tax mole.

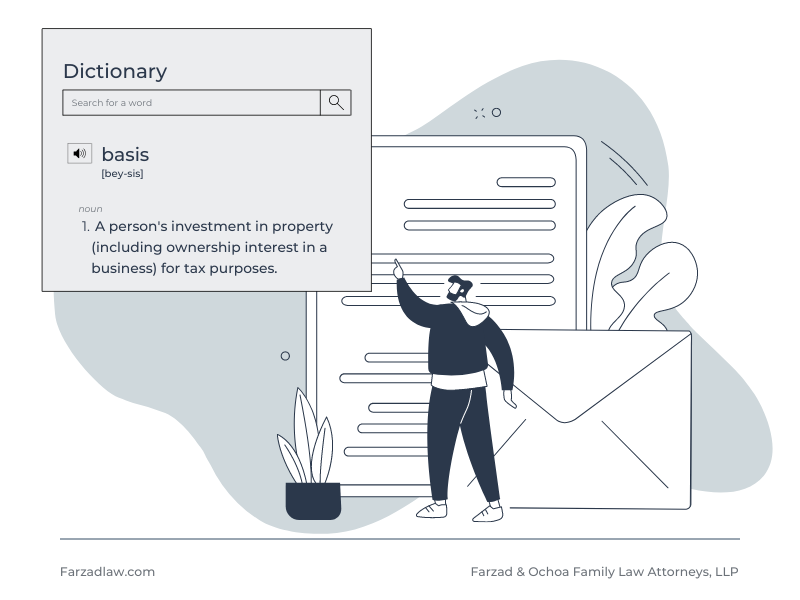

How can this be? The answer to this question lies in one word—basis

Basis is to tax deductions as oxygen is to life—the former is a necessary prerequisite to the latter.

For example, consider that for tax purposes some businesses, principally partnerships, S Corporations and Trusts operate as Passthrough Entities.

In general, the income from Passthrough Entities is reported on the tax return of the business, but it is taxed on the tax return of the owner(s).

This is all well and good when the business is passing through a profit, but if the business is passing through a loss, things can get complicated. This brings us back to BASIS. A simple definition of basis is your investment in property (including ownership interest in a business) for tax purposes.

Basis is what allows you to take deductions by virtue of the obvious fact you cannot deduct what you do not own in the first place.

Suppose you are operating a bicycle shop that is incorporated and has elected to be taxed as a S Corporation.

There are two shareholders in this corporation—yourself and one other person who we will name Fred.

You are the expert on Bicycle Sales and Service, and Fred is the one with the money and back-office skills. The company issues 100 shares of capital stock and you and Fred each purchase 50 shares for one dollar per share.

You and Fred each now have a basis in the corporation of $50, and the company has $100 in the cash register.

Since a bicycle shop requires more than $100 to operate, Fred funds the company with an additional $75,000. Now Fred's basis in his S Corporation stock is $75,050 ($75,000 + $50).

Suppose after the first year of operations the bicycle shop has a loss of $20,000. Since the company is a S Corporation this loss will pass through to each owner in proportion to their stock ownership. Because you and Fred each own 50% of the stock you will each be allocated a $10,000 loss.

Assuming he otherwise qualifies, Fred will be able to deduct the entire $10,000 on his tax return, and his basis in the stock will be reduced by the $10,000 loss he deducted, calculated as follows:

- Beginning Stock Basis: $10

- Additional Paid in Capital: $75,000

- Loss allocation ($10,000)

- Ending basis: $65,010

Since Fred has enough basis to absorb the $10,000 loss, he is allowed to deduct it on his tax return. On the other hand, since your basis is limited to the $50 you paid for the stock, your deduction is limited to $50.

However, there is some good news—the remaining $9,950 of unused loss can be carried forward and used when you have sufficiently restored your basis either via your share of profits the company earns, additional capital contributions, or other items that are deemed to increase basis.

This brings us back nicely to how legal fees incurred in connection with a divorce can still be deductible

As previously mentioned, it is settled law that amounts spent to retain or acquire property can be capitalized and added to the cost basis of the asset.

Depending on the nature of the asset, these expenditures (which include legal fees) might be deducted in the form of depreciation deductions, or they might be realized when the asset is sold because increases in basis decrease taxable gain.

However, increasing the cost basis of assets also may have immediate tax benefits in the case of pass-through entities such as S Corporations and Partnerships.

Suppose for example you are a shareholder in a S Corporation, and you are battling with your former spouse over ownership of the S Corporation stock.

Your basis in the stock is $10,000 and your share of the company's loss is $50,000 in the current year. You spend $75,000 in legal fees to retain ownership of the stock which immediately increases you stock basis to $85,000 ($10,000 + $75,000).

Therefore, you are able to immediately deduct the entire $50,000 pass-through loss and have $35,000 basis ($85,000 - $50,000) remaining. Without the addition of the $50,000 legal fees to the stock basis your deductible loss in the current year would be limited to the $10,000 preexisting basis.

There are yet other ways divorce related legal fees may be immediately deductible

Take for example the case of Liberty Vending Inc. v. Commissioner (75 T.C.M [1998], T.C. Memo-198-177).

While the taxpayer was in the hospital recovering from a heart attack, his wife filed for divorce and obtained a temporary restraining order against him, as well as an ex parte order that gave her emergency possession of the business and placed the bank accounts in escrow under court supervision.

Then in a raid worthy of a Viking sacking a 9th century monastery she showed up at the business premises with her boyfriend, fired all the employees, took large quantities of cash and equipment, removed the corporation's books and records, and changed the locks.

The taxpayer learned of his wife's pillage while he was still in the hospital and remarkably did not have a second heart attack.

Instead, he effectuated his release, obtained a lawyer, and went about regaining control of the business. In the meantime, the business teetered on the brink of disaster as invoices went unpaid and obligations were not fulfilled.

Eventually the court issued an order returning control of the company to the taxpayer. The taxpayer's attorneys continued their attempts to regain possession of the corporate assets from the taxpayer's wife and her boyfriend. The same attorneys also represented the taxpayer in his divorce action.

Upon audit, IRS disallowed the deduction of all of the legal fees on the basis that these expenses related to the taxpayer's divorce proceedings, and therefore were non-deductible personal expenses (IRC Section 262a).

Conversely, the taxpayer contended that Liberty Vending was entitled to deduct as ordinary and necessary business expenses the portion of the legal fees attributable to regaining control of the corporation.

He further contended that the legal fees were deductible because they were incurred for the management, conservation, or maintenance of property held for the production of income (IRC Section 262a).

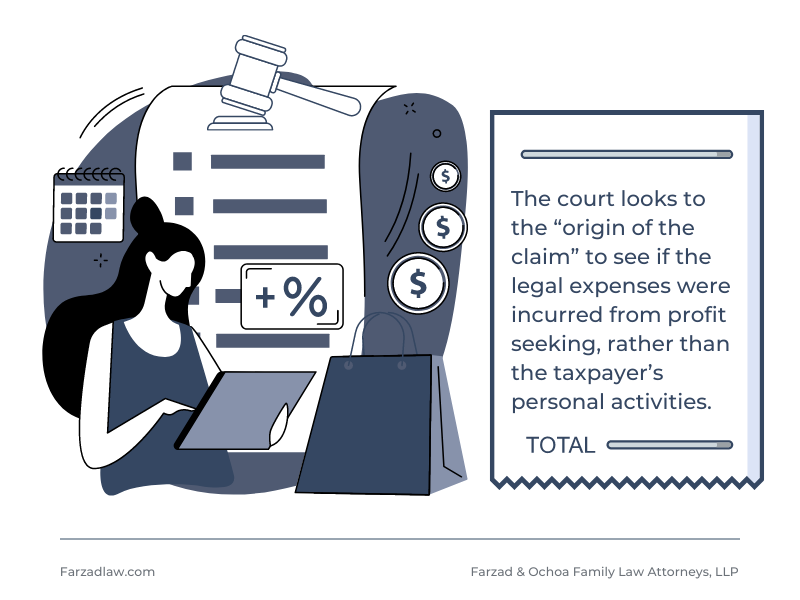

In reaching its decision, the court looked to the "origin of the claim" to see if the legal expenses were incurred from profit seeking, rather than the taxpayer's personal activities (United States v. Gilmore [63-1 USTC 9285]).

The court pointed out that while the protective order was in place, employees were fired, the company's creditors were not paid (and could not be paid without the divorce court's permission), and service obligations were not fulfilled.

Thus, the corporation's profit seeking activities were curtailed. Since the taxpayer's legal fees were incurred for the purpose of establishing his right to possession of, or participation in, the income of the company, such expenses arose from the taxpayer's profit seeking activities and are therefore deductible (see also Dolese v. United States, [79-2 USTC 10th Cir. 1979] wherein the court held that legal expenses of a corporation arising out of a divorce proceeding were tax deductible, to the extent that the cost were incurred to resist actions that interfered with the actions of the corporation).

However, the court did make it clear that the taxpayer was only entitled to deduct legal fees relating to the protective order, which should serve as a reminder that in such cases, it is important that legal fees are itemized.

The guest post author, David Ellis, is a practicing CPA in Pasadena California. He can be contacted at (626) 577-4404 or visit his CPA firm's website Ellis & Ellis CPAs to learn more. This article is for informational purposes only and is not a substitute for tax advice from a qualified professional. The author, David Ellis, CPA, and Farzad & Ochoa Family Law Attorneys, LLP assume no liability whatsoever in connection with its use. No advisor/client relationship exists between the author and the reader or Farzad & Ochoa Family Law Attorneys, LLP and the reader.